A lot of London move quotes look similar at first glance. Same number of movers, same van size, same date, then one comes in noticeably cheaper, and it's tempting to book it before the slot goes.

One of the biggest hidden differences is often the goods in transit insurance. This isn't the policy section for the van itself. It's the part that relates to your belongings while they're being moved.

For anyone moving from a flat in E14, a terrace in W4, or an office in EC2, that detail matters more than most quote forms make clear. If cover is optional, and in the UK it is, then price alone doesn't tell the full story.

Understanding goods in transit insurance for your move

When a customer compares removal quotes, the assumption is usually that every professional mover is pricing the same thing. In practice, that's not always true. One quote may include proper insurance for the contents being carried, while another may leave that point vague or treat it very narrowly.

Goods in transit insurance covers loss, theft, or damage to goods while they are being transported. In the UK, it is not legally mandatory, but it's widely regarded as a critical safeguard because it protects goods from collection to delivery, rather than protecting premises or the vehicle itself.

Why does this matter when quotes vary

Please note: if a quote is much lower, ask what protection sits behind it, not just what vehicle is included.

For a London house move, the risks are ordinary rather than dramatic. Boxes shift. Furniture gets handled through narrow halls. Items are carried down communal stairs, through lifts, into loading bays, then across busy roads. A proper removal plan assumes things can go wrong and puts cover in place for the transit stage.

What a customer should ask straight away

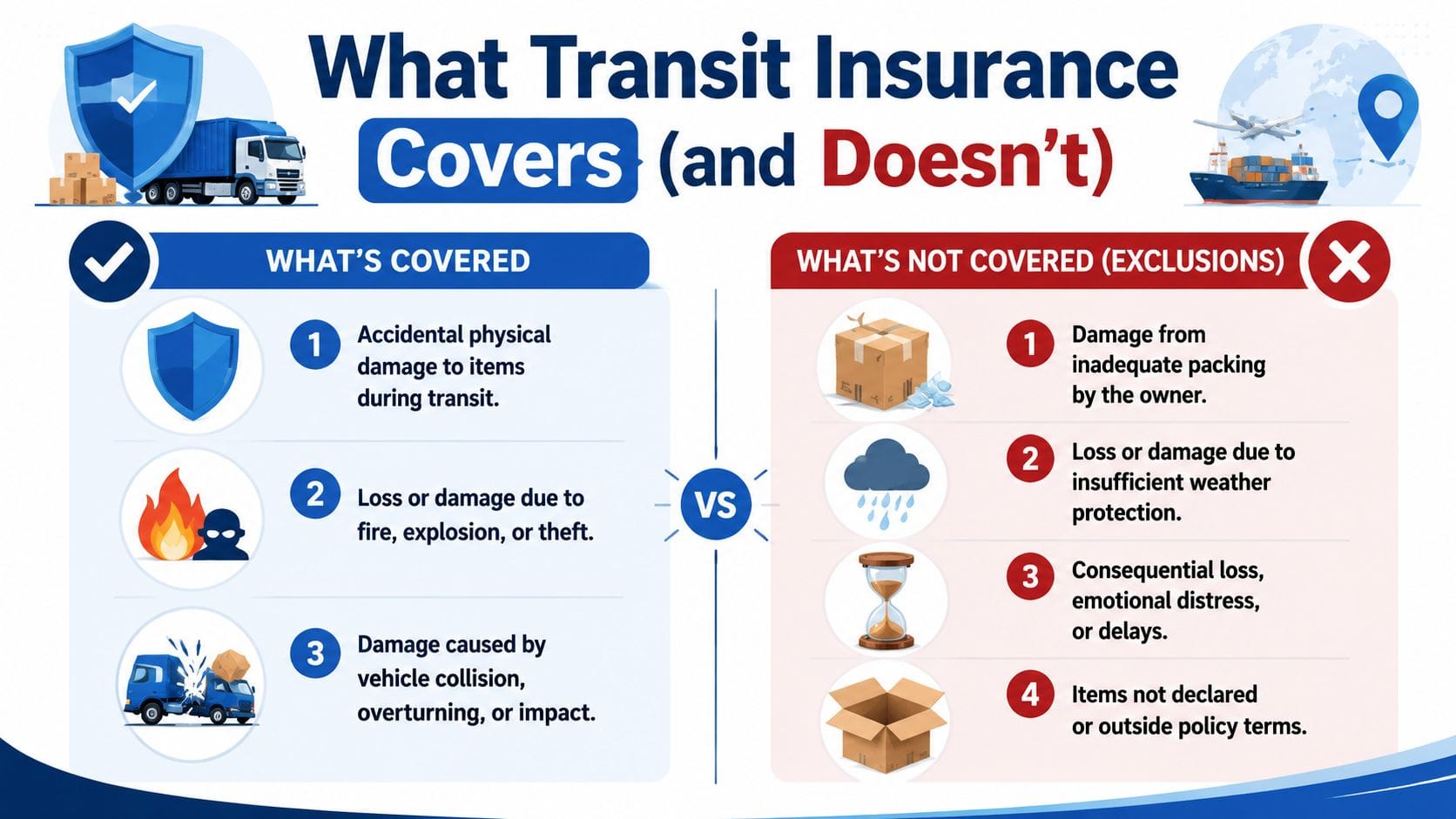

What is and is not covered by transit insurance

Customers often hear the words "fully insured" and assume that means every possible issue is covered from the moment packing starts until the last item is placed in the new home. Insurance rarely works that broadly.

For removals, one of the most important distinctions is that the goods in transit cover is separate from the vehicle policy. The van policy insures the vehicle. Goods in transit insurance relates to the contents being carried, and cover typically applies only while those contents are in transit.

What is usually covered

What often falls outside it

Why does self-packing need a direct conversation

Many customers pack at least part of the move themselves. That's completely normal, but it creates a real insurance question. If the contents were not packed securely, the removal company's goods in transit policy may not respond in the way the customer expects.

This is especially important for glassware, monitors, artwork, lamps, and anything awkwardly shaped. For smaller jobs booked on a flexible basis, such as a single-room move or a handful of larger items, the right question isn't just "are you insured?" It's "What exactly is covered if I've packed the boxes myself?"

Goods in transit is not public liability

Customers also mix up transit insurance with public liability insurance. They are not the same.

Public liability is about third-party injury or damage. For example, if a mover damages a communal wall or someone is injured during loading, that sits in a different area from the cover for the customer's goods in the van. When something goes wrong on moving day, the answer depends on exactly when it happened, what caused it, and which policy is meant to respond.

How to check a removal company's insurance

The easiest time to check insurance is before paying a deposit. Once the booking is in place, customers are far less likely to push for clarity, especially if the move date is close and access arrangements in places like Westminster, Islington, or Camden already feel complicated.

A professional answer should be calm, specific, and easy to verify. If a company has cover, it should be able to explain the type of insurance held, the limit, and how a customer can see confirmation.

Questions worth asking every mover

What a good answer sounds like

A solid response usually has three features. It names the policy type clearly, it states the cover limit without hesitation, and it doesn't mind providing documentation.A weaker response is often vague. Phrases like "everything's covered" or "don't worry, we've never had a problem" are not substitutes for policy details.

Ask for documents, not reassurance. A careful mover won't be offended by that.

Small signs that deserve attention

Cover limits and protecting high-value items

Why rough estimates can cause problems

Customers often describe a move as "just a two-bed flat" or "only a small office". That helps with vehicle planning, but it doesn't say much about value. A compact flat in Kensington, Fulham, or Hampstead can contain jewellery, designer furniture, artwork, music equipment, and multiple high-end screens. A small office in Soho can hold laptops, monitors, specialist kit, and archived files that would be expensive to replace.

If those items are not declared properly, the policy limit may not match the actual exposure. That's where underinsurance becomes a practical problem rather than an insurance term.

Items that should always be flagged in advance

What protects the customer best

The strongest position is usually created before the move starts. A survey, a written inventory, and a realistic conversation about high-value items all help align the move with the actual risk. That matters particularly for unusual or delicate loads, including upright and grand pianos.

Customers don't need a perfect household valuation. They do need a sensible one. If there is any doubt that the standard cover limit reflects the contents being moved, the right step is to raise it before booking, not after a problem appears.

London moves and making a claim

Claims are easiest to handle when the customer knows what to do on the day. The key is speed and clarity. If something is damaged, lost, or appears to have been affected during the journey, the customer should report it promptly to the removal company and keep the evidence simple and organised.

London adds its own complications. A move in Barnet can involve tight residential streets and awkward reversing space. A move in Westminster may depend on a booked bay suspension and a narrow time window. In Canary Wharf, the whole job may depend on goods-lift slots, concierge rules, and loading bay access. Those details don't mean a claim is likely, but they do explain why organised operators build insurance and process into the job.

What to do if something goes wrong

Why quote prices can reflect insurance reality

What helps a claim run more smoothly

Claims usually become difficult for one of three reasons. The first is delay. The second is missing paperwork. The third is confusion about whether the issue happened inside or outside the transit window.

Customers can improve their position by keeping the quote, inventory, and any declared high-value item notes together in one place. That makes it much easier to answer questions quickly if an insurer or removal company needs supporting information.

Your final insurance checklist before booking

Before accepting any quote, it helps to pause and check the protection behind the price. Most customers spend more time comparing van sizes than comparing cover, even though the cover is what matters if something goes wrong.

A useful final checklist:

This guide is intended as general information about goods in transit insurance and how to check cover when booking a removal company. It is not insurance or legal advice. For confirmation of cover relevant to a specific move, ask the removal company directly and request written documentation.