Buying a home in London often starts with the agreed price and a rough idea of the deposit. Then the wider moving costs come into view. Legal fees, survey costs, mortgage charges, packing, removals, and then the one that catches many buyers off guard: Stamp Duty Land Tax.

That surprise is common, especially when someone is comparing flats in Croydon, family houses in Ealing, or larger homes in Richmond and assumes the tax works as a single percentage. It doesn't. That misunderstanding can throw off a moving budget at exactly the point when decisions need to be clear.

A buyer planning a move in areas such as Walthamstow, Islington or Ruislip usually isn't asking for tax theory. The question is simpler: how is stamp duty calculated, and what does that mean for the total cash needed before moving day. Getting that right matters because SDLT sits alongside the deposit and legal work as an upfront cost, not an optional extra to deal with later.

This guide covers Stamp Duty Land Tax for residential property in England and Northern Ireland, which share the same SDLT system. If you're buying in Scotland, the equivalent tax is Land and Buildings Transaction Tax. If you're buying in Wales, it's Land Transaction Tax. Both work on a similar sliced-band principle but use different thresholds, so the figures in this guide apply specifically to England and Northern Ireland purchases.

A guide to understanding your stamp duty bill

A common pattern appears when buyers get close to making an offer. They've checked monthly mortgage payments, spoken to the solicitor, and started thinking about moving dates. Then someone mentions stamp duty, and the numbers suddenly feel less straightforward than the estate agent's listing suggested.

In London, where purchase prices can move quickly from one band to the next, that confusion has real consequences. A buyer looking at a flat in Lewisham one week and a house in Ealing the next may be dealing with a very different tax bill, even before the first box is packed. The issue isn't just the amount itself. It's when that cost needs to be available and how it affects the rest of the moving budget.

Practical rule: treat stamp duty as part of the move budget from the start, not as a last-minute legal extra.

The reassuring part is that the calculation follows a clear structure. Once a buyer understands that SDLT is charged in slices of the purchase price rather than as a single flat rate on the total amount, the picture becomes much clearer. That makes it easier to budget for removals, storage, if needed, and other costs that arise around completion.

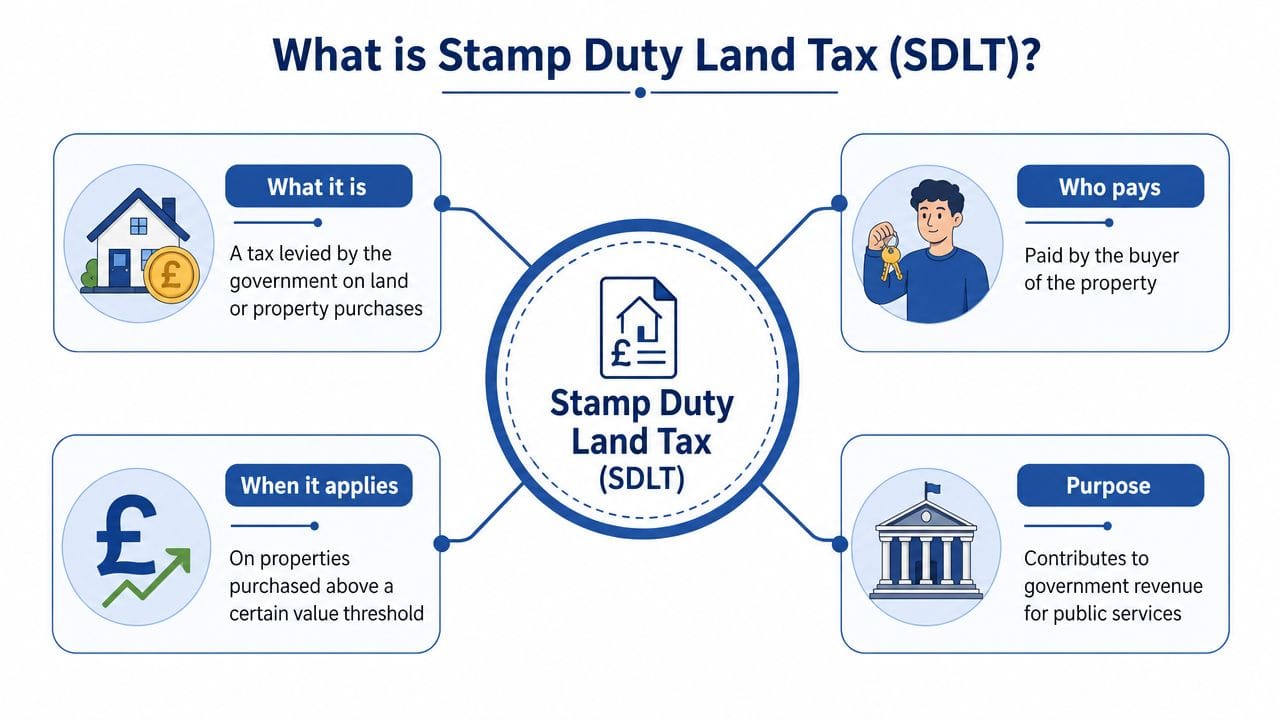

What is Stamp Duty Land Tax

Stamp Duty Land Tax, usually shortened to SDLT, is the tax a buyer pays when purchasing property or land in England and Northern Ireland. It sits separately from the deposit, the mortgage, and the solicitor's own fees. In practical terms, it's one of the key sums that has to be budgeted for before a move can happen smoothly.

Many buyers assume the tax works like a single percentage applied to the full purchase price. That's the wrong way to think about it. A better comparison is income tax. Different portions of the purchase price fall into different bands, and each band is taxed at its own rate.

The point most buyers need to grasp

Why landlords and investors need to read the rules more carefully

How stamp duty is calculated with current 2026 rates

The standard residential bands

A worked example using a purchase price of £300,000

Where buyers go wrong

The usual mistake is applying one rate to the full purchase price. A £250,000 home is not taxed at 2% across the whole amount. The first £125,000 is exempt from SDLT, and only the next £125,000 is taxed at 2%, resulting in an SDLT bill of £2,500.

The second mistake is planning for the purchase but not for the move around it. In London, SDLT can sit alongside the deposit, solicitor's costs, mortgage fees, removals, packing materials, temporary storage, and overlap costs if the buyer is leaving a rental or managing a chain.

Treat SDLT as completion money. If it is missing from the budget, every other moving decision gets tighter.

Worked examples for typical London property prices

Once the tiered method is clear, the next step is applying it to the kind of prices buyers see across London. The figures below use common London scenarios rather than abstract textbook examples. The boroughs are only there to make the examples feel familiar. The tax is still calculated by band, not by location.

Example one: a flat in Croydon or Lewisham at £350,000

Example two: a family home in Walthamstow or Ealing at £750,000

Example three: a larger property in Richmond or Islington at £1.2 million

Common stamp duty reliefs and surcharges you should know

A buyer can calculate the standard SDLT bands correctly and still budget the wrong amount for completion. In London, that happens most often where reliefs or surcharges apply, because the purchase price alone does not settle the bill.

The points that most often change the figure are first-time buyer relief, the higher rate for an additional property, leasehold rent rules, shared ownership, and the non-UK resident surcharge.

First-time buyer relief

Additional property surcharge

Buyers who already own another residential property will usually pay an extra 5 percentage points on top of the standard residential rates. In practice, this catches buy-to-let purchases, second homes, and some onward movers who have not yet sold their existing home by completion.

This is often the surcharge that most sharply disrupts the moving budget. Buyers tend to focus on the deposit, legal fees, and removals, only to realise late in the process that keeping hold of one property, even for a short period, can significantly change the SDLT position. In London, where purchase prices are already high, that extra charge can absorb money that had been set aside for storage, repairs, or furnishing the new place.

If a buyer hasn't sold their previous main residence by the day they complete on the new property, the higher rate may apply at completion. Buyers who go on to sell their previous main residence within 36 months of completing the new purchase can usually apply for a refund of the surcharge, so it's worth checking the refund rules with a conveyancer if the timing applies.

Leasehold rent rules

Leasehold purchases can bring a second SDLT calculation on the rent as well as the premium. If the net present value of the rent over the life of the lease exceeds £125,000, SDLT is charged at 1% on the amount above that threshold. This rent calculation doesn't apply to existing assigned leases; it applies only to new ones.

This does not affect every flat purchase, but it should never be waved through as a minor detail. Buyers of leasehold property should ask their solicitor to confirm exactly whether the SDLT estimate covers only the purchase price or also includes any tax due on the lease rent. That check matters more in London than many buyers expect, because flats make up such a large part of the market.

Shared ownership

Non-UK resident surcharge

Some residential purchases by non-UK residents face an additional 2% SDLT surcharge in England and Northern Ireland, on top of any other rates or surcharges that apply. This isn't simply about nationality; it's based on HMRC's specific residence tests for the transaction, broadly whether the buyer has spent at least 183 days in the UK in the 12 months before the purchase.

Anyone buying from abroad, returning to live in the UK, or buying jointly with someone whose residence position differs from their own should have this checked by a solicitor before relying on a rough estimate, since the rules apply to each buyer and can affect the whole transaction.

A relief that no longer applies

Multiple Dwellings Relief is sometimes still mentioned in older articles or calculators as a standard option for buyers purchasing more than one dwelling in a single transaction. It has been withdrawn. HMRC abolished the relief for transactions completing on or after 1 June 2024, aside from a limited set of transitional cases. If a calculator or guide still lists it as available, that's a sign the source needs to be checked against current rules.

Reliefs and special cases that need individual advice

Putting it into practice: your next steps

Understanding the formula is useful. Turning it into a reliable moving budget is what helps.

Who handles payment

In most purchases, the solicitor or conveyancer deals with the SDLT submission and payment as part of the completion process. SDLT returns must be filed and the tax paid within 14 days of completion. Buyers should still read the paperwork carefully. An estimate isn't the same thing as a confirmed calculation, particularly where leasehold terms, first-time buyer status, shared ownership, non-UK residence, or an additional property surcharge may apply.

Why timing matters

Planning your move with confidence

This guide is intended as general guidance on how Stamp Duty Land Tax is calculated. It is not financial or legal advice. For advice specific to your circumstances, contact your solicitor, conveyancer, or HMRC directly.